Preparing for Life’s Unexpected Surprises

Life rarely goes exactly as planned. Most days follow a familiar routine. People go to work, attend school, pay bills, shop for groceries, and spend time with family and friends. Everything seems normal until one unexpected event changes the situation. A car suddenly needs expensive repairs. A family member becomes ill. A household appliance stops working. A job is lost without warning.

These situations are part of life, and they can happen to anyone.

Imagine two neighbors facing the same unexpected expense. Both need to repair their car so they can continue traveling to work. The first neighbor has no savings and immediately worries about how to pay the repair bill. He considers borrowing money or using a credit card with a high interest rate. The second neighbor has built a small emergency fund over several years. Paying the repair bill is still disappointing, but it does not create panic because the money has already been set aside for situations like this.

The difference is not luck. It is preparation.

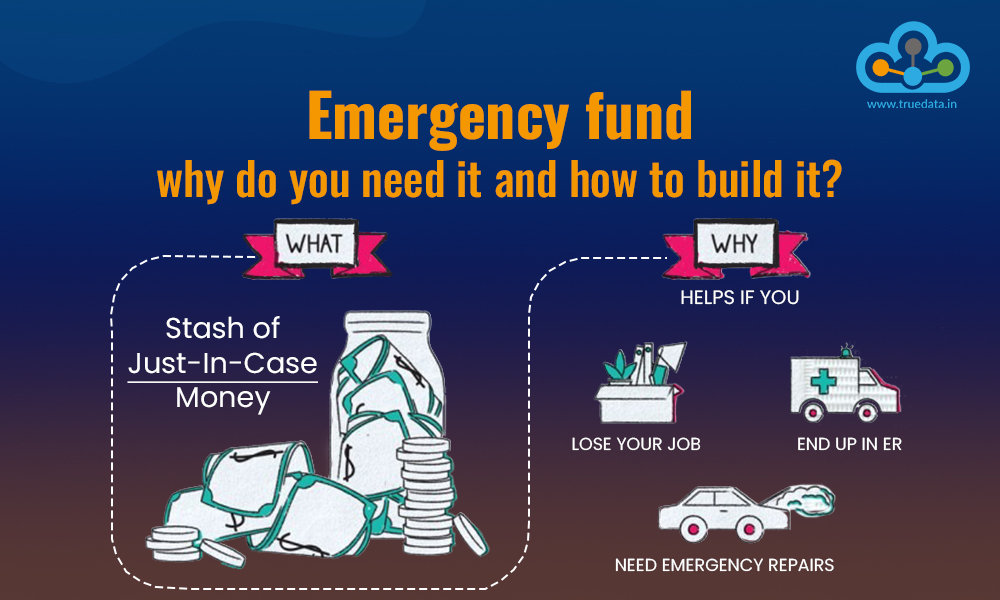

An emergency fund is money saved specifically for unexpected financial problems. It is not intended for vacations, shopping, birthdays, or entertainment. Instead, it acts as a financial safety net that protects people when life becomes unpredictable.

Many people believe they need to earn a large income before they can build an emergency fund. In reality, the habit of saving is often more important than the amount saved at the beginning. Even small contributions made regularly can gradually grow into meaningful financial protection.

Knowing that emergency savings are available also reduces stress. Unexpected expenses become easier to manage because there is already a plan in place. Rather than worrying about where the money will come from, people can focus on solving the actual problem.

Building an emergency fund is not about expecting bad things to happen. It is about being prepared if they do.

Understanding What an Emergency Fund Should Cover

Not every unexpected expense is a true emergency. Understanding the difference helps people protect their savings for situations that genuinely require them.

Imagine that a new smartphone is released and you want to buy it immediately. Although it may feel exciting, this is not an emergency. On the other hand, if your refrigerator suddenly stops working or your home requires urgent repairs after a storm, those situations may require immediate financial attention.

Emergency funds are designed for necessary and unexpected expenses that cannot easily be delayed.

Medical emergencies are one of the most common reasons people use emergency savings. Even with health insurance, there may still be costs for treatment, medication, transportation, or recovery that need to be paid quickly.

Temporary job loss is another important example. Finding new employment may take weeks or even months. During that time, rent, groceries, utility bills, and other essential expenses continue. An emergency fund helps cover these costs while reducing financial pressure.

Vehicle repairs can also become urgent, especially for people who rely on their cars to travel to work or care for family members. Similarly, important home repairs such as fixing a leaking roof, replacing a broken water heater, or repairing damaged plumbing often cannot be postponed.

Unexpected travel may also require emergency savings. A family emergency or urgent personal situation sometimes requires immediate transportation and accommodation costs.

Because emergencies are unpredictable, many financial experts recommend building enough savings to cover several months of essential living expenses. However, this goal should not discourage beginners. Even saving enough to cover one small emergency is an important first step.

The purpose of an emergency fund is not to eliminate every financial challenge. Instead, it provides valuable time and flexibility to make thoughtful decisions without immediately relying on expensive borrowing.

Building Your Emergency Fund One Step at a Time

Many people delay building emergency savings because the final goal seems too large. They hear recommendations about saving several months of expenses and assume it is impossible.

Imagine filling a large glass with water using only a small cup. At first, progress seems slow, but with patience and consistency, the glass eventually becomes full. Building an emergency fund works in exactly the same way.

The most important step is simply getting started.

Setting aside even a small amount each month creates a positive financial habit. Some people choose to save a fixed amount from every paycheck before spending on anything else. Others automatically transfer money into a separate savings account each month. Automation often makes saving easier because it removes the temptation to spend the money first.

Keeping emergency savings separate from everyday spending accounts can also be helpful. When the money is not immediately visible during daily shopping, people are less likely to use it for non-essential purchases.

Unexpected extra income can also help build the fund more quickly. Tax refunds, work bonuses, birthday gifts, freelance income, or money earned from selling unused belongings can all be added to emergency savings instead of being spent immediately.

Reducing a few unnecessary expenses may also create room for regular savings. Preparing meals at home more often, limiting impulse purchases, or reviewing unused subscriptions can free up money without making major lifestyle changes.

It is important to celebrate progress rather than focusing only on the final goal. Saving the first few hundred dollars or reaching the first month’s living expenses represents meaningful achievement. Every contribution strengthens financial security.

Using the emergency fund wisely is equally important. Once money is withdrawn for a genuine emergency, rebuilding the fund should become a priority as soon as finances allow. This keeps the safety net ready for future unexpected events.

Patience is essential throughout the process. Emergency savings usually grow gradually over months or years, but every small deposit brings greater financial confidence.

Creating Financial Peace of Mind for the Future

Money cannot prevent emergencies from happening, but it can reduce the financial stress that often accompanies them.

Imagine receiving an unexpected phone call about a family emergency. Instead of immediately worrying about how to pay for travel or other urgent expenses, you know that you have prepared for situations like this. The problem still exists, but the financial pressure is much lower because you planned ahead.

This peace of mind is one of the greatest benefits of an emergency fund.

Emergency savings also help people avoid unnecessary debt. Without savings, many unexpected expenses are paid using high-interest credit cards or loans. Over time, borrowing can make a temporary problem much more expensive. Having emergency money available often prevents this cycle from beginning.

An emergency fund also supports better financial decision-making. People who lose their jobs, for example, may have more time to search for suitable employment instead of accepting the first available position simply because they need immediate income.

Building emergency savings also strengthens other financial goals. Once this safety net is in place, people often feel more confident about investing, saving for retirement, buying a home, or starting a business because they know they have protection against unexpected setbacks.

It is important to review the emergency fund from time to time. As income, family size, or monthly expenses change, the amount needed for financial security may also change. Regular reviews help ensure that savings continue to match current needs.

No emergency fund is built overnight. It grows through many small decisions made consistently over time. Every deposit, no matter how small, increases financial stability and reduces future uncertainty.

Life will always include unexpected moments. Some challenges are small, while others are more serious. Although no one can predict exactly when these situations will occur, everyone can prepare for them.

In the end, an emergency fund is much more than a savings account. It is a source of confidence, security, and peace of mind. It allows people to face life’s uncertainties with greater strength, knowing they have prepared for the unexpected. By starting with small, regular savings and remaining consistent over time, anyone can build a financial safety net that provides lasting protection and supports a more stable and confident future.